Impact of the Middle East Conflict on Inbound Travel to Germany

Regular GNTB Market Updates on the Iran Conflict

Status: July 21, 2026 (replaces the versions of July 8, June 11, 2026, June 1, 2026, May 13, 2026, May 8, 2026, May 4, 2026, April 22, 2026 and April 21, 2026).

The German National Tourist Board (GNTB) is responding to the escalation of the military conflict in the Middle East and its potential impact on inbound tourism to Germany with comprehensive measures. A dedicated crisis task force has been established to coordinate the continuous analysis of data on current developments. The weekly monitoring reports form the basis for intensive exchange with stakeholders, partners in the German and international travel industry, political actors, and cross-border tourism organizations.

With the signing of the Memorandum of Understanding between the USA and Iran on 15 June 2026, transit routes through the Strait of Hormuz are partial-ly reopening and there is a prospect of a peace deal. The crude oil price has fallen signifi-cantly. The price for a barrel of North Sea Brent fell on 8 July 2026 to around USD 77.72, while the US WTI grade fell to around USD 73.67.

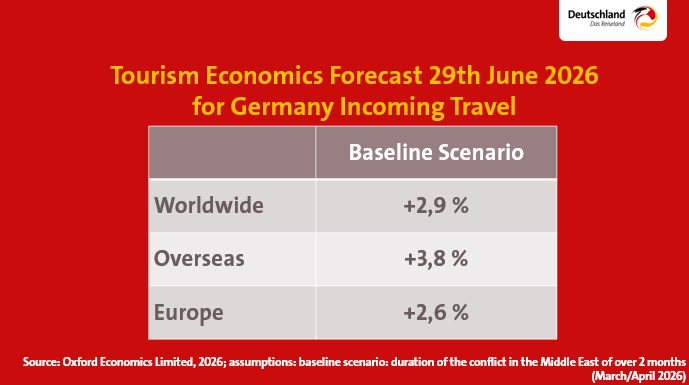

Oxford Economics raised its forecast for overnight stays by foreign guests in Germany in 2026 from +2.6% to +2.9% (2026 compared with 2025 in each case). Expected growth in overnight stays by European guests in Germany in 2026 is +2.6%, while overnight stays by overseas guests in Germany are expected to grow by +3.8%.

[Update of 21 July 2026]: The implementation of the ceasefire has repeatedly been sub-ject to serious violations, again creating a high level of risk in the Gulf region. The crude oil price is rising and on 21 July 2026 stands at USD 89.67 for a barrel of North Sea Brent and USD 82.79 for a barrel of US WTI.

[Update of 21 July 2026]: Due to the renewed escalation of the conflict between the USA and Iran, the European Union Aviation Safety Agency (EASA) is calling on airlines to avoid the airspaces of Bahrain, Kuwait, Qatar, the UAE and parts of the Gulf of Oman. This new safety warning initially applies until 29 July 2026 (Conflict Zone Information Bulletin CZIB-2026-07).

[Update of 21 July 2026]: According to surveys by the Federal Statistical Office, overnight stays by foreign guests in Germany in May 2026 amounted to 7.5 million, 0.7% below May 2025. For the cumulative period January to May 2026 compared with January to May 2025, overnight stays by foreign guests amounted to 28.7 million, 0.2% above the same period of the previous year.

The GNTB Travel Industry Expert Panel – a B2B survey regularly covering more than 200 key accounts and CEOs of international travel industry companies with business involv-ing Germany – shows a decline in the assessment of the current business situation fol-lowing the outbreak of the Middle East conflict; however, the assessment of future busi-ness development (+46) in the Q2/2026 wave is at the same level as the previous year’s Q2/2025 figure.

[Update of 21 July 2026]: In a survey of tour operators, wholesalers,

OTAs and DMCs conducted by the European Tourism Association (ETOA), published on 10 July 2026, more than four fifths of respondents report continued at least moderate business impacts of the Middle East crisis on tourism business. Declines in demand remain relevant, while cancellations, later bookings and price risks are also gaining im-portance.

In a GNTB-exclusive survey conducted in 15 countries, 55% of international travellers worldwide indicated that they would book closer to departure due to the Middle East conflict.

As part of its Economic Impact Research, WTTC forecasts global growth of the tourism sector of 3.2% in 2026. For Europe, European GDP growth in 2026 is expected to reach only 1% due to continued inflationary pressures and economic uncertainty, while travel and tourism GDP is expected to grow by 3.6%. According to the report, international visi-tor spending across Europe is expected to increase by 7.1%. Travel and tourism are ex-pected to support 376 million jobs worldwide by 2026, equivalent to one in nine jobs globally.

With its publication of 2 June 2026, UN Tourism revised its assessment of the develop-ment of worldwide international arrivals in 2026 due to the Middle East conflict from the previous 3%-4% to 2%-3%. For 2026, this would correspond to a volume of international arrivals of approximately 1.56 to 1.58 billion.

For the first quarter of 2026, UN Tourism reports a 2% increase in international arrivals worldwide, despite the Middle East conflict and rising uncertainty.

Market Assessment

Short-term Impact on Travel Flows Following the Military Escalation

According to analyses by Tourism Economics, 14 percent of global international transit traffic passes through hubs in the Gulf; around 28 million trips from the Middle East are affected, 60 percent of them to Europe.

In Germany, 4.2 percent of all flight arrivals in 2025 were via hubs in the Gulf states – of which 55.1% were direct arrivals from the UAE and 44.9 percent were transit passen-gers.

Looking at individual source markets, in 2025 73.2 percent of guests from the Gulf states travelled to Germany via Dubai / Abu Dhabi / Doha, as did 31.4 percent of guests from Singapore, 16 percent of Indian tourists, 6.9 percent of Chinese tourists and 4.6 percent of Japanese tourists.

[Update of 21 July 2026]: After a 39% decline in the number of flight arrivals in Germany via the Gulf hubs in March 2026 compared with March 2025, there has been a gradual improvement to -31% (April 2026 vs. April 2025) and -18% (May 2026 vs. May 2025). In June 2026, the number of flight arrivals in Germany via the Gulf hubs weakened again to -29% (June 2026 vs. June 2025).

[Update of 21 July 2026]: Seat capacities to Germany are declining particularly on flights from Saudi Arabia (-43%), the UAE (-36%), Oman (-32%), Qatar (-26%) and Kuwait (-24%), and to a lesser extent from Bahrain (-2%).

[Update of 21 July 2026]: Yamina Sofo, Director GNTB Dubai – UAE: “The GCC markets continue to rank among the highest-spending source markets for tourism to Germany and fundamentally offer considerable growth potential. At the same time, the framework conditions for inbound tourism business have deteriorated significantly in 2026. In addition to the ongoing tense security situation in the region, travel decisions are particularly affected by restrictions in air transport and the partial suspension of services by European airlines.

Against this backdrop, marketing activities in the GCC markets were temporarily suspended as a precautionary measure. Following continuous monitoring of market developments and a renewed assessment of the prevailing conditions, market activities have gradually resumed.

While Gulf carriers continue to provide a large share of the direct flight connections to Germany and play a key role in maintaining accessibility, the outlook for inbound tourism business over the coming months remains highly uncertain. A sustainable recovery will require not only further stabilization of the security situation but also reliable and predictable air connectivity. Until then, subdued demand, short-term booking decisions and generally muted market development are expected.

Under the current circumstances, market activities in the GCC countries will continue in a targeted and situation-specific manner. The focus is on selected measures that can be implemented effectively despite the existing uncertainties. These include, in particular, digital B2B and B2C marketing activities, ongoing cooperation with media, trade and distribution partners, as well as close engagement with airlines and tour operators. Subject to prevailing conditions, participation in the Arabian Travel Market (ATM) in September 2026, together with seven German partners and an accompanying press conference, is planned. In addition, a roadshow in Saudi Arabia and the United Arab Emirates is scheduled for late October. [WG: Update...kt Tracker | Outlook]

The implementation of these measures will continue on an ongoing basis, taking into account both the current security situation and market developments."

Economic Impact

On June 5, 2026, the EU Commissioner for Transport and Tourism, Apostolos Tzitzikostas, stated that he sees no signs of a jet fuel shortage in Europe in the coming months. However, high fuel prices are prompting airlines to discontinue unprofitable routes.

The European Commission adopted guidelines for the EU transport and tourism sector in response to ongoing fuel supply disruptions and the closure of certain air and maritime routes related to the Middle East crisis. The guidelines focus on aviation and specifically address the potential impact of jet fuel shortages should the conflict continue.

The EU Commissioner for Sustainable Transport and Tourism, Apostolos Tzitzikostas, stated on 24 June 2026 that the Iran war, which broke out in ear-ly March, had had a significant impact on global travel activity and had once again shown how important resilience is.

OECD Europe ranks first among import regions dependent on the Middle East. The Middle East has typically supplied up to 375 thousand barrels per day, or 75% of Europe’s net jet fuel imports. In April 2026, North America and Africa (Nigeria) are replacing parts of jet fuel imports from the Middle East.

[Update of 21 July 2026]: According to an analysis of data from Amadeus/ForwardKeys, no increase in average base fares for flights to Germany excluding taxes and surcharges can be identified in June 2026 compared with June 2025 for the USA, China and Japan. For flights from India, a price increase is clearly visible in June 2026, as it was in the pre-vious month (+8.8% June 2026 vs. June 2025).

As in the previous month, there is a clear increase in the price level for flights from the UAE to Germany: this stands at +28.8% for June 2026 vs. June 2025. Price increases are also visible for flights from Kuwait (+20.7%), Oman (+4.5%) and Israel (+2.7%), but not for Bahrain (-6.6%) and Saudi Arabia (-10.7%).

At the same time, petrol prices have also risen so sharply that the industry must expect an impact on travel costs for car trips in Europe. With a share of 44 percent in the modal split, the car is the main mode of transport used by European travellers to Germany.

Airlines, including Lufthansa, are cutting capacity. According to The Guardian, around 2 million airline seats worldwide were removed from May flight schedules. The reasons are sharply increased kerosene prices and greater planning uncertainty. According to Cirium data, around 13,000 fewer flights are expected to operate in May; globally, this represents less than 2% of capacity, but it may be clearly noticeable on individual routes and at specific hubs.

It is currently impossible to assess how logistics costs in maritime transport, including fuel, insurance and risk optimization of transport routes, will affect trade in goods in the medium and long term.

A looming global economic crisis caused by disrupted logistics chains could also weak-en tourist flows through declining purchasing power in affected source markets. Howev-er, there are currently no reliable indicators for this. Experts differ in their assessment of when the reopening of the Strait of Hormuz will lead to a revival of the global economy.

Shifts in Travel Flows and Market Segments

Resilience of German Inbound Tourism

Approximately 77% of international overnight stays in Germany are generated by European source markets. In addition, intra-European travel demand is expected to increase in 2026 as a result of the current conflict. European Travel Comission data indicates a rise in intra-European travel intentions by five percentage points compared to the previous year.

21 July 2026]: In an update of this survey, conducted from mid to late May 2026, 64.5% of European travellers chose to travel within Europe.

This is supported by an initial Appinio study commissioned by the GNTB, which shows increasing travel intent to Germany from key source markets such as the Netherlands and Belgium.

From Israel, restrictions in air traffic are leading to sharply declining overnight stays in Germany. Following an analysis of connectivity and flight data and assuming a conflict duration of four months, the GNTB expects a decline of around 18% for 2026 compared with the previous year.

Stable Demand on Online Travel Platforms

[Update of 21 July 2026]: For search volume for Germany during the period from 28 Feb-ruary 2026 to 21 June 2026, Expedia recorded almost stable search demand compared with the same period of the previous year (-0.3%), putting Germany above the search volume for Europe (-2.4%). Bookings in Germany for this comparison period show sta-ble revenues (+2.9%) despite lower overnight stays (-0.4%).

Conclusion

The military conflicts in the Middle East are having both direct and indirect effects on inbound tourism to Germany.

Opportunities for Germany as a travel destination in international competition are based on its positive image as a safe, high-quality destination and the current trend toward intra-European travel.

Among European competitors, Germany benefits from a very competitive price level. According to MKG Consulting, hotel prices in Germany averaged €100 during the first four months of 2026, down from €103 in the same period of the previous year and significantly below the price levels of competing destinations such as France, Italy, Switzerland, Spain, and Austria.

Overall, there are realistic chances that declines from the Middle East can be structurally offset by visitors from Europe and overseas markets such as the USA, China, Japan, or India. Previous crises have already demonstrated the high resilience of inbound tourism due to its broad market diversification.

Provided there is no further escalation of conflicts and no global economic crisis emerges, German inbound tourism could once again prove to be resilient.

Up until the outbreak of the Iran conflict, the GNTB had projected growth in global inbound tourism to Germany of +3.2% for 2026, based on the assumption of a stable geopolitical environment without sharp increases in oil prices or inflation.

Updated projections by Tourism Economics (June 29, 2026) reflect scenario-based adjustments in line with current developments:

Overseas

- High economic relevance despite a low volume share of 1.5 percent of Germany incoming tourism: guests from the GCC generate around EUR 3.0 billion in reve-nue and spend on average about twice as much as the global average.

- High structural dependency: 73.2% of flight arrivals from the UAE to Germany are routed through these hubs

- Significant market correction: GNTB forecast for 2026 adjusted from +5% to -14% (current overnight stays January–April 2026 vs. January–April 2025: -19%)

- Travellers are placing greater emphasis on flexibility and value for money, reflect-ed in shorter booking windows, refundable fares and alternative routes.

- At the same time, demand is increasing for new travel formats such as longer stays and combined leisure and remote-work concepts.

- Postponement of ATM to 14–17 September 2026: The planned participation will be adjusted accordingly to the new date in summer. The concrete format is cur-rently being coordinated closely with the trade fair and the German partners.

- • [Update of 21 July 2026]: Against the backdrop of current developments, the GNTB is continuously assessing the situation in the GCC markets and deciding on further market activities on a day-to-day basis. The aim is to maintain Germany’s market presence and deploy marketing budgets responsibly.

- Israel is experiencing severe disruptions in air traffic, leading to a decline of 75% in passenger arrivals and a 79% reduction in seat capacity.

- Against the backdrop of the severely restricted market situation, the GNTB is closely monitoring further developments and maintaining continuous exchange with local key accounts in order to identify market changes at an early stage and enable rapid reactivation once conditions stabilize.

- Asian markets show a differentiated but overall stable development. Demand remains intact but is more volatile than in Europe or North America and reacts more sensitively to external shocks.

- China and India show strong momentum at the beginning of the year, with continued growth expected for 2026.

- Schengen visa applications from China increased by 20% in the first quarter of 2026 compared to the first quarter of 2025.

- Different levels of dependence on Middle Eastern hubs: China (6.9%) and Japan (4.6%) are only minimally affected and benefit from stable, broadly diversified flight connections via direct routes and alternative European hubs. India, with a share of around 16%, shows significantly higher dependence, but can at least partially mitigate the impact through alternative direct connections.

- Alternative connections from India to Germany departing from Indira Gandhi International Airport, Chhatrapati Shivaji International Airport Mumbai, and Kempegowda International Airport Karnataka.

- Indirect impacts affect all markets: longer routes, reduced capacity, and higher prices are slowing booking dynamics and increasing demand for direct connections.

- The focus of the GNTB market activities is on close monitoring of market developments and ensuring continuous presence. At the same time, exchange with relevant key accounts is being intensified in order to identify market changes at an early stage and respond flexibly.

- A study by market research firm MMGY from February 2026 shows that international travel intent among U.S. travelers is at a multi-year high: 36% of active U.S. leisure travelers plan to travel abroad within the next six months—the highest level since before 2020.

- North American markets remain robust. Connectivity and demand remain stable, supported in part by the positive development of air connections between Europe and North America.

- Operational feedback shows no decline in demand or significant cancellations. Bookings and existing travel plans remain stable. However, customers are taking more time to make booking decisions.

- The USA and Canada recorded a good start to the year for overnight stays in Germany (+1.8% USA, +4.8% Canada) and continued stable connectivity.

- Stability factor target group structure: Travelers to Germany from the upscale segment are less sensitive to economic uncertainties and demonstrate comparatively stable travel intentions.

- Due to stable demand, the GNTB is focusing on further leveraging potential in North America, particularly through targeted outreach to the upscale segment. At the same time, close cooperation with key accounts is being maintained in order to secure existing bookings, support conversion, and generate additional demand impulses.

Europe

- [Update of 21 July 2026]: In June 2026, air fares from Spain to Germany in-creased: according to an analysis of data from Amadeus/ForwardKeys, average base fares excluding taxes and surcharges for flights to Germany rose by 1.5% compared with June 2025. From the UK, they declined in June 2026 compared with June 2025 (-4.0%).

- Implications for GNTB market activities: targeted communication of Germany’s strong value for money compared to competing destinations, along with an increased focus on promoting rail travel as an attractive alternative.

- The Netherlands and Belgium remain key source markets for stabilizing inbound tourism to Germany during the crisis: a GNTB study from March shows increased travel intentions to Germany in the Netherlands from 32% (September 2025) to 37% (March 2026), and in Belgium from 17% to 23%. This is already reflected in overnight-stay figures for the first four months of 2026 (Netherlands: +3.4% year to date, Belgium: +2.8%).

- Rising transport and energy costs remain a burden: higher flight prices due to jet fuel costs as well as increasing cost pressure in car travel (44% share). However, Germany benefits from strong rail connections to key nearby markets.

- In response, the GNTB has been strengthening communication in nearby markets since the end of April through a high-reach Expedia campaign, “Next Stop Travel Destination Germany.” In Austria and Switzerland, the marketing of bus travel is also being specifically intensified.